25th March 2026 “Both sides of the BNG coin” seminar

Part 1 – Currently available support for farmers and landowners

1. Current Government support

One of the reasons, arguably the most important reason, why there was enough interest in setting up a BNG project to host this seminar, is the diminished and unreliable level of Government support for agriculture.

With Single Farm Payments and the Basic Payment Scheme, every year, without fail, from 2005-2023, eligible farmers and landowners have received area-based Government support for keeping land in agricultural condition. For 18 consecutive years around 97% of the total agricultural land in England claimed these payments.

Such consistency provided a safety net for farmers and landowners – a buffer against the unexpected and uncontrollable.

Ironically, it is these two words – unexpected and uncontrollable – that perhaps most aptly describe Government support since 2023, the final year of the basic payment

This table shows a selection of different forms of Government funding from the last 6 years – with green indicating when each scheme was open to applications, and red when they were closed. This is not a comprehensive selection but should cover the more widely available schemes for the average farmer or landowner.

What this table hopefully makes obvious at first glance, is not only how the availability and variety of funding has decreased, but also how it has become more sporadic. What were previously regular application windows have become inconsistent. The best illustration of this is the SFI, which as I am sure all of you are aware, was meant to be Defra’s flagship scheme in the post-BPS scene, yet shut unexpectedly on 11 March 2025, and will have been shut for 14 months by the time it reopens in June 2026.

2. SFI 2026

Application windows:

• June 2026 – farms under 50 ha and farms not in an existing ELM agreement.

• September 2026 – all farms.

• 31 actions removed.

• Only 1 agreement per SBI number.

• AHW7: Enhanced overwinter stubble added to the 25% area cap options.

• £100,000 per agreement per year cap introduced.

• Area of rotational actions cannot be increased beyond what it was in year 1.

• Adjusted payment rates.

• SFI management payment removed.

In spite of its unreliability, and really highlighting how desperate the situation has become, SFI still remains the primary source of Government funding, and the 2026 application windows, in June and September, will be a key calendar date for those not currently holding an agreement.

It is also worth giving a brief moment to the actual figures involved – as well as the intention of this funding and its accessibility. Yet again, for the most part this is not a pretty picture, although I should say that it is hard to reliably comment, in such general terms, on the change in payment rates because income from SFI is dependent on a number of variable factors, including but not limited to:

• Farm size

• Farm enterprise

• Locality

• Environment

• Willingness to participate

• Other available alternatives

However, as an illustration of how payment rates may have changed, I will now lay out a couple of

example schemes for a hypothetical farm – starting with BPS as a baseline.

3. SFI vs BPS

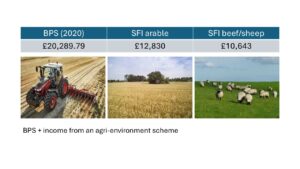

The average farm size in England is 87 ha. In 2020, before BPS began to be phased out, on non Severely Disadvantaged land the BPS payment rate was £233.22 per ha. On 87 ha this comes to a total of just over £20,000. This payment was for keeping the land in agricultural condition and observing Greening and Cross Compliance requirements.

Basic Payment Scheme Example

• Average English farm size = 87 ha

• 2020 BPS payment rate = £233.22 / ha

=£20,289.79

From 2021 onwards BPS payments were tapered as the beginning of there being phased out.

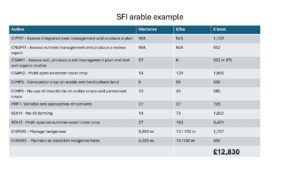

In comparison to this, a relatively standard and unobtrusive option for an arable system is displayed above. On the 87 ha example this would produce almost £13,000.

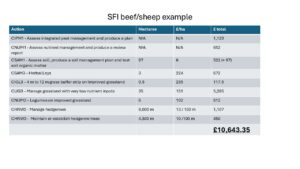

Taking the same standard approach for an 87ha beef/sheep enterprise, you would be looking at around £10.5 thousand.

In both of my examples, the annual income from SFI is less than that received from BPS, even with high reduction, and the requirements for receiving the funding are greater. On top of this, where BPS was simply linked to hectarage, income achievable through SFI will be dictated in the first order by what is on the ground in each individual holding. This will impact certain enterprises and farming systems more than others.

To further add to this, where BPS could be stacked with the previously available agri-environment schemes, such as countryside stewardship and environmental stewardship, SFI stands alone as the sole provider of area linked payments in the current situation.

What I hope the above has made clear is that Government funding for farmers and landowners in 2026 is not what it was even 3 years ago – in terms of value, reliability, and availability.

The combined effect of the dire tale I have just run through, is that farmers and landowners are now looking for alternate sources of funding. Including BNG and two of the other more well-established Natural Capital options – Nutrient Neutrality and Woodland/Peatland Carbon.

David Marrow would be pleased to hear from you if you have any queries or questions. 01392 823935 or email bng@townsendcharteredsurveyors.co.uk