“Both Sides of the BNG Coin” – Seminar 25th March

PART 4 – ANALYSIS OF THE BNG MARKET

How was the current BNG market created?

The BNG market has been a long time in the making. Starting out with the foundational influence from the 2010 Lawton Review “Making Space for Nature” shaping BNG policy in England.

Key milestones:

- 2010 Lawton Review, “Making Space for Nature” foundational for Mandatory BNG in England

- 2012 National Planning Policy Framework and Inaugural Biodiversity Metric 1.0

- 2016 Brexit Referendum

- 2020 Agriculture Act – moving away from EU subsidies and more towards agri-environmental schemes in England.

- 2021 Environment Act (primary BNG legislation)– air, water quality, protect wildlife etc- “public money for public goods” - Amended Town and Country Planning Act 1990 inserting schedule 7a – 10% BNG need.

- The image below shows the cover of the first book published as a “UK Environmental Credits User Guide” in 2021. It charts the lead up to BNG and other Natural Capital markets.

- 2021 DEFRA’s Eftec analysis used estimated values of £20-25,000 per unit.

- 2022 TCS Habitat Distinctiveness/”Rarity” Pyramid was published, see page 4 ,5 and 10.

- There were voluntary BNG schemes in a limited number of local planning authorities (LPAs).

- 2023/4 BNG – Secondary legislation - Statutory Instruments becoming a mandatory national framework for all LPAs on12th February 2024 with small sites included on 2nd April 2024.

- This created a National BNG Framework with local LPA add-on policies.

There still remain the outstanding results from DEFRA consultations from last summer. Although an announcement in parliament last December made clear that small sites of less than 0.2 ha will be exempt form BNG requirements, at some point in the future. We also await the Nationally Significant Infrastructure Projects (NSIP) to come online – to be included in BNG – from May this year.

A common question – who is who in the BNG world – who are we talking to and taking advice from?

Understanding the market requires knowing who is involved and who you are talking to; Defra in 2023 mentioned only two BNG brokers and operators. Three years on this is Hugh Townsend’s list:

Key Actors

Defra in February 2023 mentioned only two – BNG operators and brokers.

BNG Operators

- DIY Landowner of habitat bank, individual consultants’ advice as needed. Separate ecologist and solicitor for s106 & CC.

- DIY Landowner using BNG project manager/consultant joined up advice on BNG marketplace, ecology, estates, agricultural/grants, stackability, legal, insurance and tax. Cost usually <5% of value of units.

- BNG Landless Operators 1. The “pay nothing now but pay more later” with variable packages – Operator taking 25-95% of gross sale value. Free habitat bank set up costs for ecology and s106/CC legal costs, operator can control sales or own them out right and can make the landowner’s payments annually over the 30 year term.

BNG Brokers

1. “The Pure broker” – similar to an estate agent, works on commission – no need to commit to other services – unregulated or RICS regulated – independent no agenda behind the scenes i.e. bond holders or lenders to the brokerage business or with other affiliations.

2. Part of the Landless operators’ package selling units. Or units owned outright by Landless operator. Brokers affiliated with landless operators, and those integrated with ecological, forestry or other service providers.

3. Part of other businesses - an investment house, an ecologists, foresters or other ecological service.

Others

- Insurance brokers for BNG projects

- Investors/wealth managers

- Specialist mortgage brokers

- Ecologists

- Solicitors

Townsend Chartered Surveyors

An independent RICS regulated “one stop shop” with a joined up and continuous service to create a habitat bank with our own team of panel ecologists, solicitors, foresters. Making use of our 40 years of marketing such assets combined with our rural estate management experience. Modular advice also offered. And if also instructed separately the national leading pure broker of units.

Nature of BNG Units and Trading Rules

There are 150 different habitat types split into 17 broad habitat types and 5 distinctiveness/rarity tiers. Not all can used for sales. What BNG units can be traded is determined by the habitat type and tier, with rules allowing “trading down” the TCS distinctiveness pyramid under specific conditions—for example, higher-tier habitats can offset losses of the same or lower tiers, while very high-tier habitats require exact matches or bespoke agreements with Natural England. Spatial weighting multipliers (100%, 75%, 50%) affect the number of units used in a sale.

Complexity of Habitat Bank creation and the expert input required

BNG projects require multidisciplinary expertise. From ecologists, solicitors (notably specialist drafting is required by planning lawyers for s106 agreements and conservation covenants), tax experts, insurance brokers, and (if needed) specialist mortgage brokers. We cannot emphasise enough the importance of a coordinated team and a holistic approach, noting that ecological knowledge alone is insufficient without a commercial yet cautious and well thought through approach with experience and understanding of the BNG market and legal process.

The success of a project will heavily rely on market knowledge from the outset and when designing the habitat bank. TCS are and have advised on over 90 habitat sites throughout England and have a panel of nationwide ecologists and solicitors aligned with our approach. As land agents we are used to managing property projects with a team of experts. The biggest advantage using TCS is you will have the same pair of eyes on the project from the first telephone /Teams call right through to the sign-off of the S106 or conservation covenant.

Phasing and Valuation of Habitat Banks

Our phasing strategies for habitat banks range from a single-phase, fixed phases, multiple small phases to a full flexible phase approach, which we are promoting to be only created on a phase by phase basis at the point when units are sold.

This type of initiative is the hallmark of the added value we strive to obtain for our clients.

The valuation of BNG units and land is challenging due to limited comparables, variation across local authorities (due to spatial weighting), and the fact that the market is still immature. My opinion is the land value will typically decrease by 80-90% after unit sales but should start to increase again during the 30-year term. The RICS is currently forming a Experts Working Group to give guidance on the valuation of BNG and land which I am looking forward to working on.

However, I find that Real-time market prices (or handshake deals) at the point sales are agreed, are critical for accurate BNG market assessment, in what could be a fast-moving market with prices always shifting.

What is being sold?

There are 150 different habitat types split into 17 Broad Habitat types. You cannot trade to mitigate loss between the area, lineage and water course habitat types. There are 5 different Distinctiveness/Rarity Tiers. Not all habitats can be used for sales.

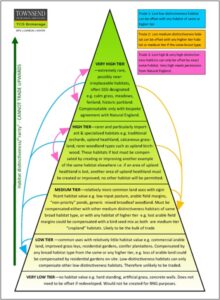

| TCS Habitat Distinctiveness/”Rarity” Pyramid published 1.12.2022 |

Infographic showing how different distinctiveness habitats can be used for offsetting. Very Low Distinctiveness habitats cannot be used for offsetting and currently do not require it if lost. Low Distinctiveness habitats can only offset other low distinctiveness habitats, and can be offset by any habitat of the same distinctiveness or higher. Medium Distinctiveness habitats can offset any low distinctiveness habits, or medium distinctiveness habitats of the same broad type (arable, woodland, grassland etc), and can be offset by medium distinctiveness habitats of the same broad type or any habitat of higher distinctiveness. High Distinctiveness habitats must be offset by the exact same habitat in a different location (e.g. upland birchwood can only be offset by more upland birchwood), and can offset losses of the same habitat elsewhere or any medium distinctiveness or low distinctiveness habitat. Very High distinctiveness habitats behave in the same way as high distinctiveness habitats, except that offsetting them requires special permission from the Secretary of State. This system therefore suggests the best prices for any unit from any LPA area will most likely only be achieved if marketed nationally.

Four stages of market development

We believe that the BNG market should evolve through four stages:

- The first was the Pre-mandatory voluntary market which involved only a few LPAs and fragmented policies.

- The second is the Start-up stage with the mandatory market post-February 2024. I believe we are still in this stage.

- The third will be the scale-up stage. We have seen some green shoots of growth from mid-2025. We placed £7m worth of sales in the last two quarters of 2025 and enquiries have in 2026 increased by 233%. In 2025 our average running lot size was 16 units and the current running lot size is 11 units.

- The fourth will be the mature stage which will feature a transparent, efficient market with all habitats available and reduced transactional costs.

Currently, in our experience, the market faces challenges including lack of fluidity, a two-tier pricing between Pure Brokers and Landless Operators, unregulated activity, Local Planning Authorities being slow and the extra expense of the alternative option of using Responsible Bodies and cautious landowner behaviour.

The market is also influenced by local planning authority policies (some LPAs still do not have BNG policies in place), spatial weighting considerations, and competition amongst habitat banks nationwide.

These factors are leading to significant price disparities.

BNG Market – Overview

We have an increasing demand for a wide range of BNG lot sizes, ranging from 0.01 up to 220+ units and everything in between. As of the 10th March 2026, the average running lot size we have dealt with is 11.77 units.

Factors for increasing demand (March 2024)

Demand by broad habitat type

We have calculated what percentage of our purchasers require the habitat types listed below. The stats below do not consider the number of units required, simply whether any habitat in that broad habitat type were requested.

- 65% – Grassland

- 36% – Heathland and Shrub

- 36% – Individual Trees

- 19% – Hedgerow

- 10% – Watercourse

- 8% – Woodland and Forest

- 2% – Sparsely Vegetated Land

- 2% – Urban

- 14% Any area habitat

e.g. 65% of our purchasers will need at least some Grassland.

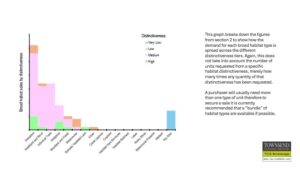

Demand by distinctiveness

This Bar Chart breaks down the figures from the slide before to show how the demand for each broad habitat type is spread across the different distinctiveness tiers. Again, this does not take into account the number of units requested from a specific habitat distinctiveness, merely how many times any quantity of that distinctiveness has been requested.

A purchaser will usually need more than one type of unit therefore to secure a sale it is currently recommended that a “bundle” of habitat types are available if possible.

Supply

Supply is constrained by the cost of establishing habitat banks and the market still being in the start-up stage. This imbalance risks price spikes. These could adversely affect developers wanting to build out a site or sell it, as they could need to BNG units at much higher prices. Landowners, especially DIY operators, may have more flexibility to wait out market troughs.

- Bottom to market price

- Drying up of supply = scarcity

- Supply lead in time is faster than Demand

- Supply is more flexible

- Supply will be less urgent in a price trough

Buyer and Seller Guidance

Vendors of BNG units benefit from using Pure Brokers who provide real-time market assessments and have extensive established networks. They should have the widest range of vendors nationally including all types of operators so knowing what is going on. This ensures that vendors achieve the maximum number of sales and the best prices.

Transactions of BNG units require careful contract management, including holding the sale money in a stakeholders’ account. Ideally a client account insured and regulated by the RICS. Confirmation of unit allocations by the Natural England Register must be provided before the broker releases the sale proceeds to the vendor unless other arrangements are made.

Demand and Supply Dynamics

Demand for BNG units is gradually increasing. A “dead cat bounce” will likely signal the BNG market has found its feet and will start the scaling-up stage. Demand will be driven by off-site units competing with the cost of on-site mitigation, on-site mitigation being more realistic and sustainable and the impact of Nationally Significant Infrastructure Projects, which will be vast, now requiring BNG from this May.

Moving plates

I have not had one case yet of a developer’s LPA turning down (although some have asked why or have mentioned the hierarchy) a purchase of units from further afield whatever the hierarchy suggests. If the units are less expensive and the LPA wants development in their LPA why would they want to discourage development?

Competing habitat banks where local economics are not comparatively as strong and there are less other options for using the land in these LPAs means their bottom price could be a lot less then on the out skirts of say London or Birmingham.

Then each farming holding has of course different land qualities what it can expect to grow and how profitable it is. Therefore, with different business priorities and aims with often family considerations and a need to consider the next generation especially where there is a family home, all comes in to play.

If in an Area of Strategic Significance such as a LNRS you can produce 15% more units than your neighbour who might not.

There are a lot of different drivers where one habitat bank will for good reason compete nationally with all others.

Another factor can be to have a quick sale to recover the initial habitat bank set up costs.

Real time market value

- Maybe often only a subtle difference but with fast moving intangible assets this can become a vital.

- TCS have always used “real-time market information” to report on market rates for intangible assets, straight from our different Trading Books. We report market prices (as we have done since 1991 in Farmers Weekly, see below, then Farmers Guardian) for BNG as the price delivered to the developer’s site and not what the vendor receives from the sale after any spatial weighting.

- Real time values of course are not formal valuations. However, when it comes to deciding on what is going on in a market, now, it can be the most important.

- Market prices can move quickly up (the echo chamber trading phenomenon) and down (for example if it is the first sale for a habitat bank and the vendor wants to recover creation costs).

- The highly leveraged Landless Operator business affect.

What does the market look like now?

- Too many third parties trying to make something out of the market. Gold rush mentality.

- Too many promises on the achievable price per unit trying to be fulfilled.

- Not fluid or efficient.

- Unregulated.

- Two tier set of prices between Pure Brokers and Landless Operators.

Market Challenges and Outlook

We have seen a lot disinformation in the market, unrealistic price expectations anchored to DEFRA’s initial estimates, and a fragmented supply chain. There is a need for a more transparent, competitive, with more regulated brokers, to improve market efficiency.

In our view, the interaction between local and national market forces, spatial weighting, and habitat distinctiveness, adds complexity to trading decisions.

And of course, we still await the results of DEFRA’s consultation and their suggested tinkering with the scheme. It is notable that current industry opinion is that the announced small site exemption of up to 0,2 ha would have only affected 3% of sales already recorded on the NE Register.

We believe that the scaling-up and maturity of the market will depend on improved on-site mitigation practices with competitive off-site unit pricing to match the cost.