The biodiversity net gain market is becoming more active. Farmers Weekly looks at the detail

The law requiring a 10% uplift in biodiversity for any new development is not expected to come into force until at least late 2023.

To meet this requirement – which can be either on-site or off-site – the developer must first try to minimise the loss of habitat on their development. The value of any habitat that is lost must be replaced, with at least 10% extra value on top. Many local authorities are already making 10% biodiversity net gain (BNG) a condition of planning permission, with some understood to be requiring as much as a 20% net gain.

Hugh Townsend, of Townsend Chartered Surveyors, is warning there are some common misunderstandings about the BNG market – one of the biggest being that land managers who generate biodiversity units are likely to be restricted to selling them within the same local planning authority (LPA).

One of the guiding principles is that developers should seek off-site BNG credits that are local to the development where practical. However, Mr Townsend says a national market for biodiversity units will have to develop, because certain types of credit may be difficult to source locally because of the way the scheme will work.

“More detail is expected on this later this year as part of the continuing consultation process,” he says. “But it is clear this will be a national, and not just a local, market. It has been suggested LPAs will have registers of what units are available for sale in their areas. But what if there are some units available locally and the vendor is offering them at too high a price?

“Does the developer have no option but to buy them if these are the only ones that work for them?

Interestingly, Defra is also saying LPAs should not be able to force developers to buy units from them, nor to charge developers for their part in the process,” he says.

“The purpose of the legislation is to see an increase in biodiversity at no cost to the taxpayer. The best way of achieving this is through an open market, to balance supply and demand without pockets of the country enforcing their own particular agenda.

“Land managers should understand that by only marketing BNG units locally or privately, they run the risk of not getting the best price.”

What are biodiversity units?

A measure of biodiversity has been devised by Defra. This quantifies the habitat that will be affected by any development into “biodiversity units”. The latest version of this is known as Biodiversity Metric 3.1.

Biodiversity units are calculated using the size of a parcel of habitat and an assessment of its quality. Quality relates to the type of habitat, its distinctiveness, condition and strategic importance. The metric uses habitat area (measured in hectares) as its core measurement, except for linear habitats, such as hedgerows, lines of trees, rivers and streams, where habitat length is used.

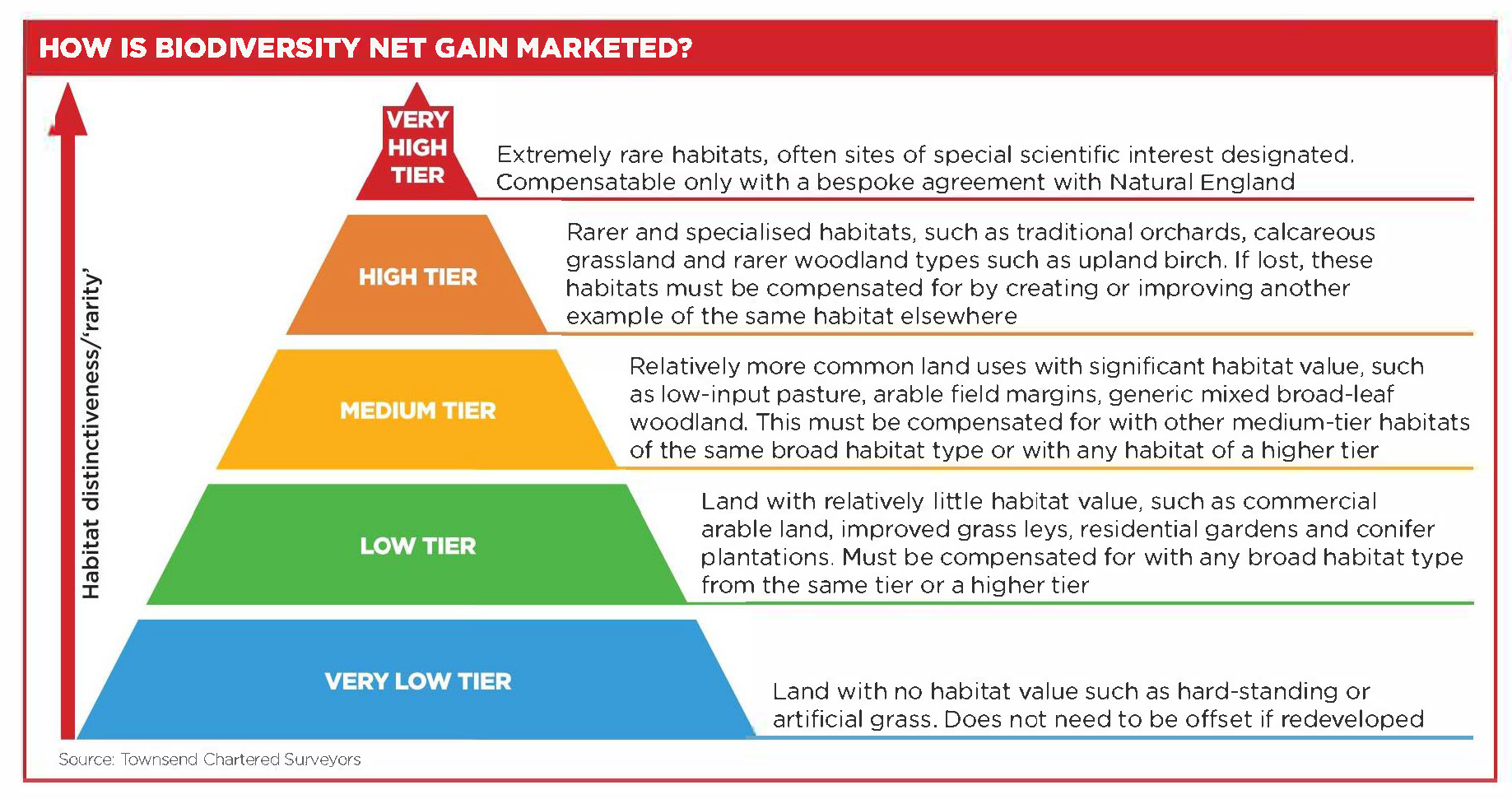

How are different types of habitat assessed?

All habitats can be categorised by “broad type” and “distinctiveness”. There are 15 types of broad habitat type, including woodlands, hedges, arable land, grassland, urban, heathland, wetland, ponds and rivers.

Within each broad habitat type there are also a number of possible options – for example, under grassland, the land may be commercial ryegrass pasture, semi-natural lowland calcareous grassland or a traditional hay meadow.

Different habitats are then classified by their distinctiveness, which means how rare and valuable the habitat is. Habitats that are the most distinctive will be worth more units and there will be tighter restrictions on how to replace them.

What does this mean for demand for credits?

An important rule is that a lost habitat cannot be replaced by a habitat that falls within a lower tier of distinctiveness, says Mr Townsend. So, it is not just a question of how large an area compensates for a lost habitat, but also what quality the replacement is. Development will be most common on land that falls within either the low- or medium distinctiveness level.

It is not anticipated that farmers will trade many low-distinctiveness units, as most land is already low distinctiveness or higher.

The bulk of trade is expected to fall into the medium tier, where biodiversity units will be created based on new habitat creation on intensively farmed arable and pasture or by enhancing poor-condition habitats, such as low-quality woodland.

In practice, a developer carrying out a residential development on an arable field (low distinctiveness) may be able to make up for a significant proportion of the lost habitat on-site, just through the creation of gardens for the houses in the new development. The remainder, plus the 100/4 net gain, might then come from paying for medium-tier units.

Will developers be particular about the types of habitat they look for?

The guidelines state that where medium-tier land is lost to a development, it will need to be replaced with either other medium-distinctiveness habitats of the same broad type, or any habitats of high or very high distinctiveness.

This means that if building takes place on land growing a wild bird seed mix, the developer could use biodiversity units from the creation of a new buffer strip or wildflower margin, but not from improving the condition of a low-input pasture.

This is because although this would come under the same tier, it’s a different broad type of habitat. They could, however, use credits from a traditional hay meadow, because even though this is a different broad type of habitat, its distinctiveness is considered “very high”.

It becomes more complex for development in an area of high distinctiveness, where the developer must replace what is lost with the exact same type of habitat elsewhere.

So, if they have gained permission to fill in a high-priority wildlife pond as part of the development, they would need to get another pond created or improved elsewhere.

It is, therefore, expected that for some habitats in this tier there will only be small numbers of units available, as fewer farmers can offer them, making the credits very valuable.

On the downside, farmers may have to wait a long time for a buyer who needs that type of unit. “Developers will be forced to look beyond their own LPAs to satisfy this need, thus further creating the national market,” says Mr Townsend.

How many units will developers need to buy?

Defra has suggested that if the annual rate of development stays at about the same level as it has over the past 20 years, 6,330ha/year could be needed for BNG offsetting, based on Defra estimates that 1ha of development land will require 0.94 units.

Mr Townsend says as many as nine units a hectare have been generated on off-site land.

How much will units be worth?

This is an emerging market so there are no hard and fast rules. Transactions to date have been under conditions created voluntarily by individual LPAs, prior to BNG becoming mandatory. This means, at present, a transaction in one LPA can be very different to one in another.

Defra suggested in its first consultation that units may fetch between £9,000 and £12,000, however, it has since said payments may be as high as £20,000-£25,000, depending on habitat scarcity, says Mr Townsend.

This payment would cover the length of a 30-year agreement. “We have seen both higher and lower prices per unit than Defra’s predictions, but understandably developers are careful not to give away what they are prepared to pay in what [at present] is an inefficient market,” says Mr Townsend. “However, this will change when there is a fully regulated national market.” ■

To download/view the article click here